Most behind-the-curve central banks: Russia, Mexico, Indonesia… and Australia.

Quantamentry — Taylor-rule deviation snapshot, May 2 2026

Snapshot Sat May 02 2026 00:00:00 GMT+0000 (Coordinated Universal Time) · 6 min read

Most behind-the-curve central banks: Russia, Mexico, Indonesia… and Australia.

Quantamentry — Taylor-rule deviation snapshot, May 2 2026.

TL;DR

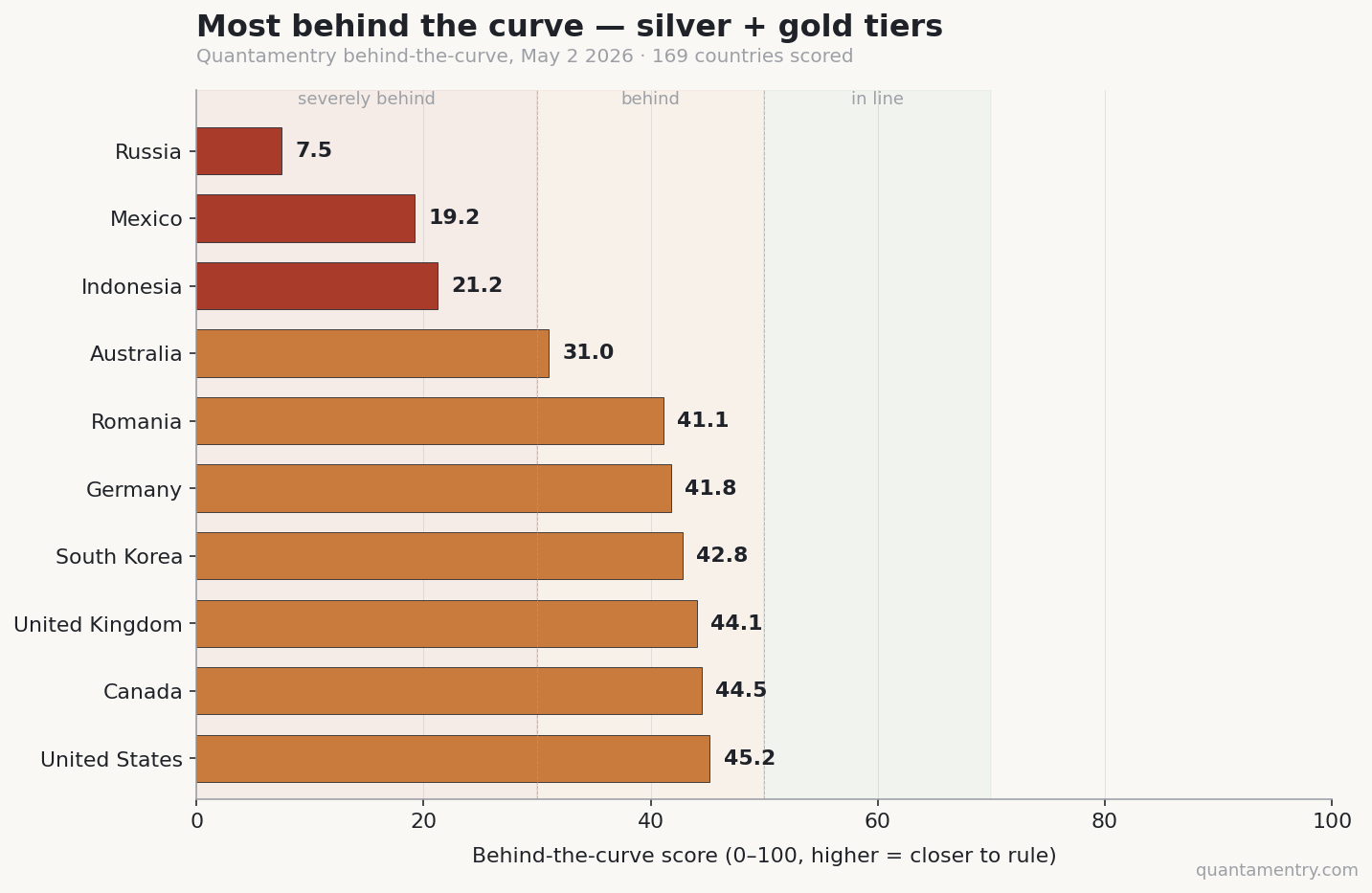

- Most behind: Russia (7.5), Mexico (19.2), Indonesia (21.2). Expected.

- Surprise: Australia (31.0) — fourth-most behind, ahead of Germany and the UK on this dimension.

- Most ahead (excessively hawkish vs the rule): Philippines (85.8), Colombia (85.8), Brazil (71.9).

- The G7 cluster between 41 and 61 — split down the middle.

The pattern: EM Asia and LatAm are running tight; G10 and EMEA are running loose. Currency markets agree.

What "behind the curve" means here

Every central bank has a model-implied policy rate at any moment — a function of where inflation actually sits versus the target, where output sits versus potential, and how persistent both deviations are. The classic formulation is the Taylor rule:

i* = r* + π + α·(π − π_target) + β·output_gap

Where:

i*= policy rate the rule says the bank should setr*= neutral real rate (estimated via HP filter on the country's history)π= current CPI (YoY, with a 3m/3m annualized fallback when YoY is missing)π_target= the bank's stated point target (or band midpoint)α,β= the standard 1.5 and 0.5 weights, applied symmetrically

We compare i* to the actual policy rate and convert the gap to a 0–100 score:

- 0–30: severely behind the curve — actual rate is far below the rule

- 30–50: behind the curve

- 50–70: in line with the rule

- 70–100: ahead of the curve (running tighter than the rule)

A low score isn't automatically bad. A central bank can credibly run "behind" when it has high confidence that disinflation is structural and short-rate cuts will avoid recession. But persistently behind = currency pressure, sticky inflation expectations, and (usually) eventually a faster-than-planned tightening cycle.

Most behind the curve — silver + gold tiers, May 2

| # | Country | BTC score | Composite |

|---|---|---|---|

| 1 | Russia | 7.5 | 34.5 |

| 2 | Mexico | 19.2 | 52.0 |

| 3 | Indonesia | 21.2 | 56.7 |

| 4 | Australia | 31.0 | 59.0 |

| 5 | Romania | 41.1 | 53.2 |

| 6 | Germany | 41.8 | 60.2 |

| 7 | South Korea | 42.8 | 61.4 |

| 8 | United Kingdom | 44.1 | 60.6 |

| 9 | Canada | 44.5 | 62.2 |

| 10 | United States | 45.2 | 66.0 |

The G7 stripe (DEU, GBR, CAN, USA) all cluster between 41 and 45. Their actual rates are below where their inflation + output gap would put them on the rule — but only modestly. The Fed at 3.625% with CPI 3.26% gives a real rate of roughly 0.4%, which is dovish for a small but positive output gap. None of these are crisis cases, but none are tight either.

Most ahead of the curve

| # | Country | BTC score |

|---|---|---|

| 1 | Philippines | 85.8 |

| 2 | Colombia | 85.8 |

| 3 | South Africa | 78.4 |

| 4 | Israel | 77.9 |

| 5 | Hungary | 74.8 |

| 6 | Brazil | 71.9 |

| 7 | Serbia | 69.0 |

| 8 | Poland | 63.8 |

| 9 | Japan | 61.3 |

| 10 | Turkey | 61.2 |

Two clusters:

- EM Asia / LatAm IT regimes running deliberately tight (Philippines, Colombia, Brazil, South Africa, Hungary, Poland) — these banks lived through the 2021–23 inflation overshoot and are keeping real rates high to anchor expectations.

- Special cases — Japan at 61 because its target is 2% and CPI just edged above it for the first time in a generation (BoJ at 0.5% nominal still scores "ahead" because the rule says "barely positive" too). Turkey at 61 because the rate is 37% with CPI ~31% — high, but our Taylor implies even higher given the rule's α coefficient on the headline gap.

Two case studies

Classic: Russia, BTC = 7.5

Policy rate 21%. CPI ~8% headline, 9-10% on persistent core. Implied Taylor rate (with r* of ~3% and π_target of 4%) is somewhere north of 25%. CBR is running below model — credibility gap also at 7.7 (essentially zero) and composite 34.5 (third-bottom on the full table). The story since 2022 is a war-time policy regime where the rate is set to defend the rouble first, manage inflation second. The Taylor rule isn't really the framework being optimized for. Our score reflects that.

Surprising: Australia, BTC = 31.0

RBA policy rate 3.85% (cut from 4.35% in late 2024 and again in early 2025). CPI YoY 2.4% (right at target band midpoint). Output gap mildly positive. Implied Taylor rate ~4.6%. The RBA is ~75 bps below the rule — not dramatic, but the surprise is who it is: the RBA's institutional reputation is for late-cycle hawkishness and slow cutting cycles. Two cuts in 14 months has put it in the same bucket as Romania and ahead of the UK on dovishness vs the rule.

The market read: AUD is 4% weaker against the USD year-to-date despite a positive carry that should have supported it. That's the mechanism — running below the rule when others (USA, NZD, CAD) are at-rule manifests as currency softness even with no formal shift in stance.

What this dimension is not

A few things worth flagging because we get them in DMs:

- It's not a direction-of-travel signal. A bank can be 30 (behind) and cutting, or 70 (ahead) and cutting. Our communication-stance dimension captures the direction; this one captures the level.

- It's not a recession indicator. Being ahead of the rule isn't always restrictive — Brazil's "ahead" reflects a long disinflation playbook, not imminent recession.

- It's not adjusted for FX regime. Pegged or managed-float economies (Saudi Arabia, Hong Kong, Denmark, etc.) get scored against their domestic Taylor rule as if they were free-floaters. That's a known limitation. We surface it in their methodology footer.

What's coming next on Quantamentry

- Next week: how we built a 169-country macro platform on free public data — the engineering post.

- Two weeks out: hawk vs dove — what 900 central bank statements scored by FinBERT and Claude Haiku reveal about the gap between talk and action.

- Soon: the Quantamentry API. Country risk and macro intelligence, REST, $49–499/mo.

If you want the daily snapshot, the historical Taylor-rule series, or early API access — [subscribe to Quantamentry]. We'll email you the moment access opens.

— Quantamentry, [publish date]