We scored 169 central banks. The G7 didn't make the top 10.

Quantamentry — sovereign credibility snapshot, April 23, 2026

Snapshot Thu Apr 23 2026 00:00:00 GMT+0000 (Coordinated Universal Time) · 5 min read

We scored 169 central banks. The G7 didn't make the top 10.

Quantamentry — sovereign credibility snapshot, April 23, 2026.

TL;DR

The most credibly-anchored monetary regimes right now are mid-sized inflation targeters and small open economies — not the majors. The G7 cluster between 59 and 66 on our composite (mid-pack). Russia and Turkey close the table at 35.

What we score

169 countries, 0–100 composite, six dimensions, daily:

- Credibility gap — distance between actual CPI and the central bank's stated target (asymmetric LINEX loss; under-shooters hit harder than over-shooters).

- Behind the curve — Taylor-rule deviation. How far is the policy rate from where output and inflation say it should be?

- Communication stance — every English-language CB statement since 2024, scored hawk/dove by FinBERT and reconciled with Claude Haiku.

- Geopolitical pressure — GDELT event flow scored for country-specific impact.

- Growth — OECD CLI + business confidence + unemployment Δ (gold-tier countries); GDP percentile + WEO deviation (silver tier).

- Liquidity — credit-to-GDP gap + DSR + real policy rate (gold); REER + FX reserves + external debt (silver).

Weighted composite (0.25 / 0.20 / 0.10 / 0.15 / 0.15 / 0.15), smoothed with a 30% trailing 90-day average for stability. Free public data only — World Bank, IMF, BIS, FRED, OECD, ILO, GDELT, Open Exchange Rates.

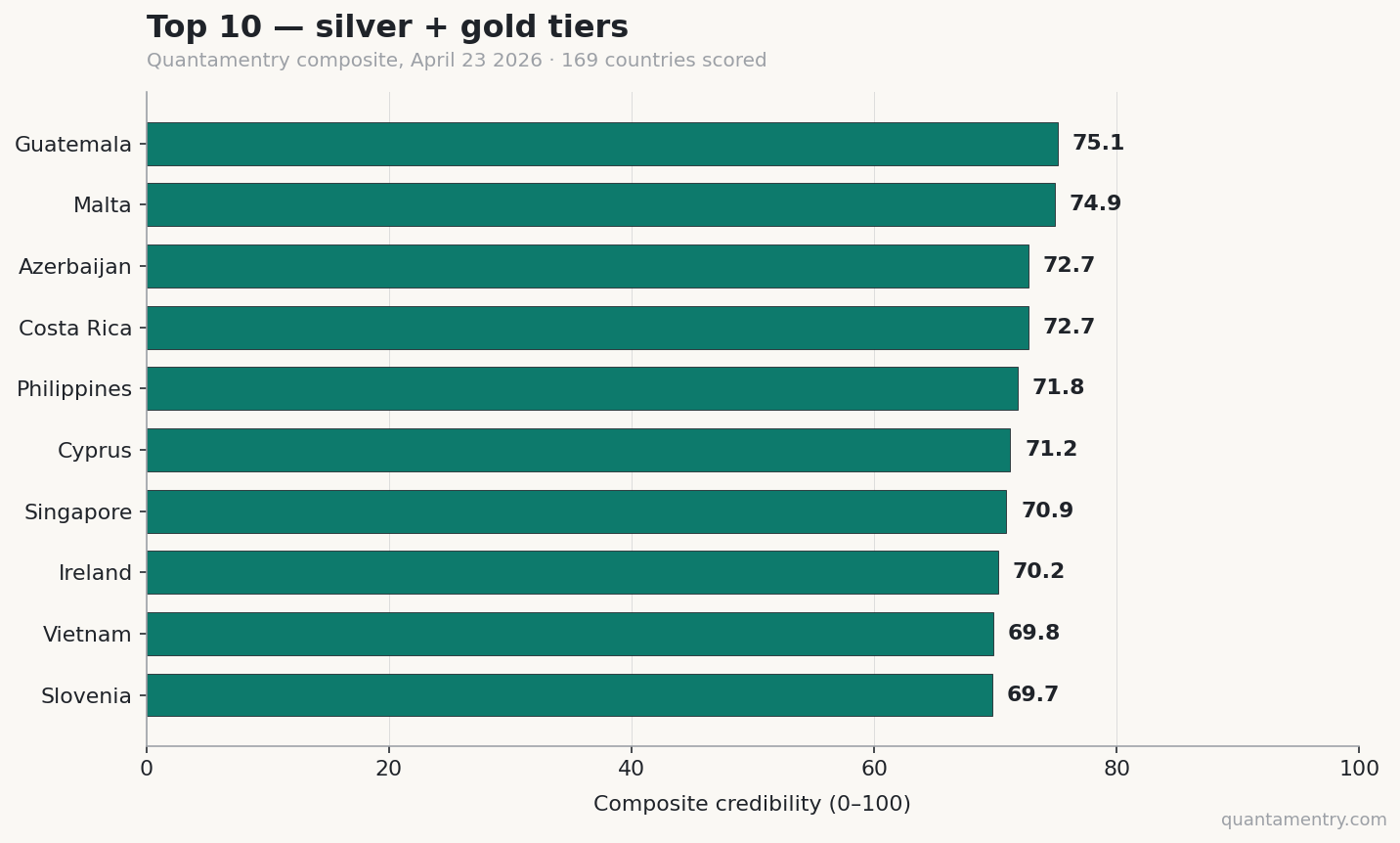

Top 10 (silver + gold tiers, April 23)

| # | Country | Score | Region |

|---|---|---|---|

| 1 | Guatemala | 75.1 | LatAm |

| 2 | Malta | 74.9 | EU periphery |

| 3 | Azerbaijan | 72.7 | Caucasus |

| 4 | Costa Rica | 72.7 | LatAm |

| 5 | Philippines | 71.8 | SE Asia |

| 6 | Cyprus | 71.2 | EU periphery |

| 7 | Singapore | 70.9 | E Asia |

| 8 | Ireland | 70.2 | EU |

| 9 | Vietnam | 69.8 | SE Asia |

| 10 | Slovenia | 69.7 | E Europe |

What's not on the list: any G7. The highest G10 entrant is the United States at 65.8 (#13). Switzerland lands at 64.7 (#14). Germany 59.4 (#27). Japan 63.0 (#23).

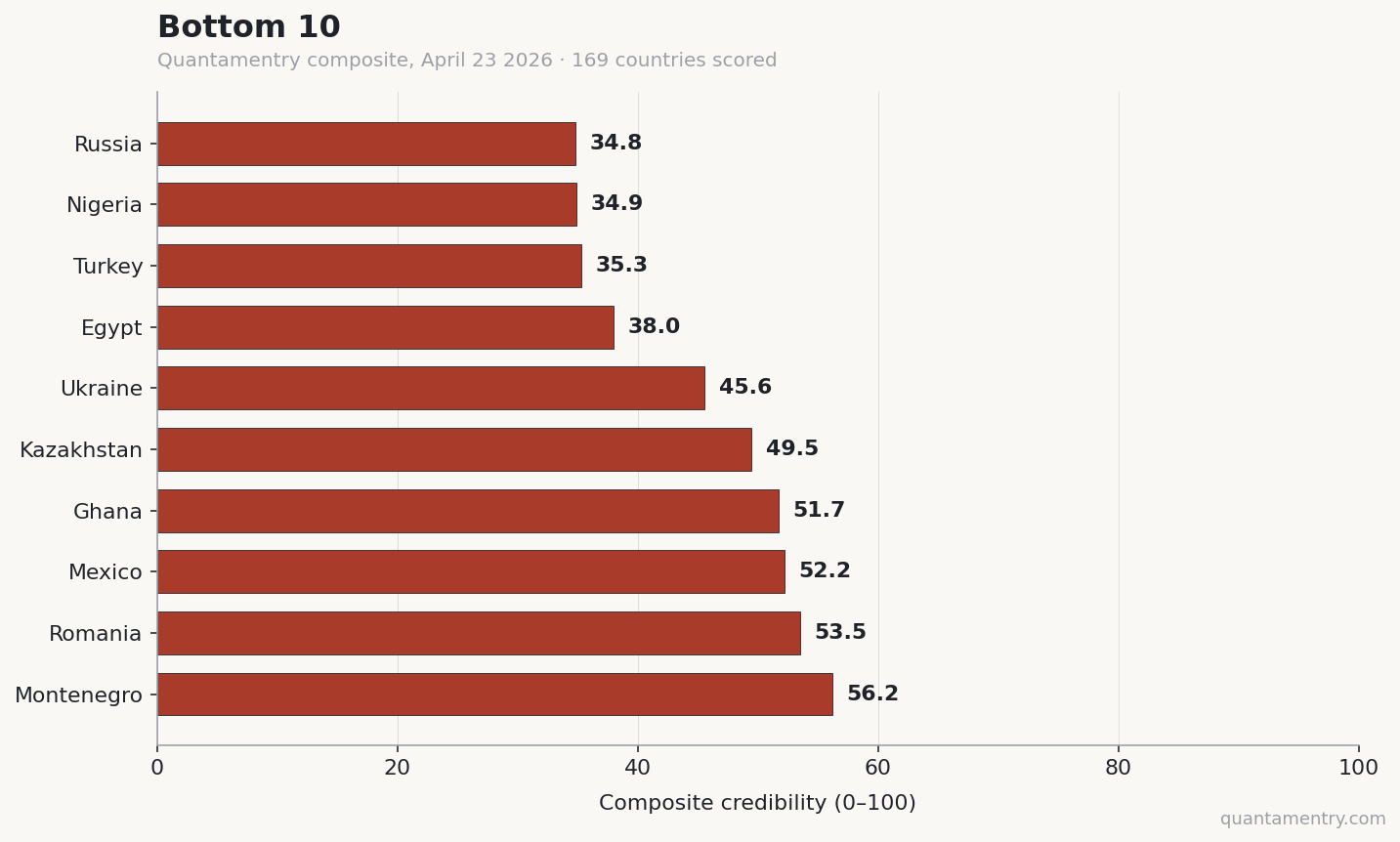

Bottom 10

| # | Country | Score |

|---|---|---|

| 1 | Russia | 34.8 |

| 2 | Nigeria | 34.9 |

| 3 | Turkey | 35.3 |

| 4 | Egypt | 38.0 |

| 5 | Ukraine | 45.6 |

| 6 | Kazakhstan | 49.5 |

| 7 | Ghana | 51.7 |

| 8 | Mexico | 52.2 |

| 9 | Romania | 53.5 |

| 10 | Montenegro | 56.2 |

No surprise at the bottom. Russia and Turkey are the long-running pair — sanctions/CPI shock and persistent unorthodox policy respectively. Mexico is the one to watch: it cracked the bottom 10 of gold-tier countries this month on a widening real-rate vs Taylor gap and a sharp peso move.

Three surprises

1. Czech Republic leads the gold tier

CNB scored 68.0 on April 23 — top of gold. Credibility gap maxed at 100 (CPI on the 2% target), behind-the-curve at 59. CNB started cutting in late 2023 and stayed close to the model-implied path since. The cleanest IT regime in our gold panel right now.

2. Brazil ranks ahead of every G10

BCB at 67.6 — second in gold, ahead of Switzerland, USA, Australia, Japan, every G10. Why:

- IPCA tracking near the 3.0% target.

- Selic well above the Taylor-implied path (behind-the-curve = 75).

- Statements consistently hawkish in our communication scoring.

- Growth dimension at 67.0 — strongest of any gold-tier country.

The "EM political risk" discount most cross-country frameworks bake in doesn't apply when you're scoring on actions, communication, and outcomes.

3. Germany at #21 of gold tier

DE 59.4. The drag is growth (40.3) and a credibility gap (89.7) just below the matched-target band. Germany inherits ECB policy that's currently tighter than its output gap warrants — a structural single-currency tension that surfaces in any common-policy framework. Not a CB judgement; a structural one.

Caveat: the bronze tier

Twelve smaller economies — Niger, Algeria, Togo, Benin, Côte d'Ivoire, Cambodia, Mali, Qatar, Senegal, UAE — score even higher than Guatemala in our model. We don't put them in the headline ranking because they have annual-only macro data, and most either lack a formal inflation target or run a peg. They live in our bronze tier with a clear data-quality flag. The tier system is how we keep "the model says X" honest about how thick the input data actually is. More on this in a future post.

What's coming next on Quantamentry

- Next week: the most behind-the-curve central banks right now — Taylor-rule deviations and what they mean for FX.

- The week after: how we built a 169-country macro platform on free data.

- Soon: the Quantamentry API. Country risk and macro intelligence, REST, $49–499/mo.

If you want the full ranking table, daily snapshots, or early API access — [subscribe to Quantamentry]. We'll email you the moment access opens.

— Quantamentry, [publish date]